Shareholders of Elevance Health would probably like to forget the past six months even happened. The stock dropped 24.6% and now trades at $308.66. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Following the pullback, is now an opportune time to buy ELV? Find out in our full research report, it’s free.

Why Are We Positive On ELV?

Formerly known as Anthem until its 2022 rebranding, Elevance Health (NYSE:ELV) is one of America's largest health insurers, serving approximately 47 million medical members through its network-based managed care plans.

1. Economies of Scale Give It Negotiating Leverage with Suppliers

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $188.2 billion in revenue over the past 12 months, Elevance Health is one of the most scaled enterprises in healthcare. This is particularly important because health insurance providers companies are volume-driven businesses due to their low margins.

2. Wall Street Expects Impressive Revenue Gains

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Elevance Health’s revenue to rise by 8.5%, an improvement versus its 10.7% annualized growth for the past five years. This projection is particularly healthy for a company of its scale and implies its newer products and services will catalyze better top-line performance.

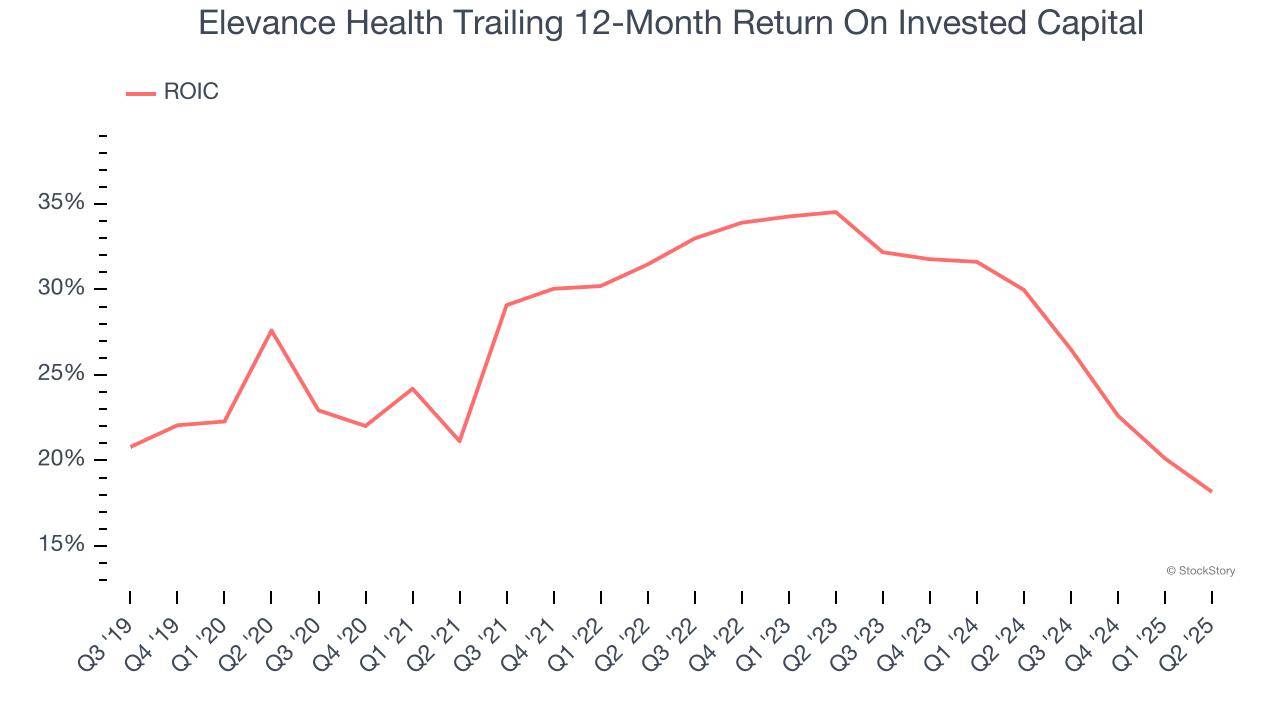

3. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Elevance Health’s five-year average ROIC was 27.1%, placing it among the best healthcare companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

Final Judgment

These are just a few reasons Elevance Health is a high-quality business worth owning. After the recent drawdown, the stock trades at 8.4× forward P/E (or $308.66 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.